Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

In the world of institutional trading, information is power. But that power has an expiration date—the moment someone else gets the same information. Real-time dark pool data gives traders visibility into the institutional layer of the market that standard platforms never show. This guide explains why the timing of that data matters, and how to use it.

Dark pools are private exchanges where institutional investors execute large block trades away from public markets. These venues allow pension funds, mutual funds, hedge funds, and large traders to execute substantial positions without immediately revealing their intentions to the broader market.

The name “dark pool” reflects the lack of transparency—trade details aren’t publicly displayed until after execution. In 2026, dark pools account for approximately 30-40% of all U.S. equity trading volume, making them a critical component of market structure that most retail traders never see.

The window for using this information closes fast. Every minute between execution and when you learn about it is a minute the market uses to react.

Historically, dark pool trades were reported with delays—sometimes 15 minutes or more. Under current FINRA Rule 6272, dark pools must report trades within 10 seconds of execution. But even that 10-second window matters in fast markets.

With delayed data, a trader might see:

Real-time dark pool platforms transform this landscape. Services like MobyTick deliver institutional flow data within seconds of execution, giving traders actionable intelligence while the print is still relevant to current price action.

With real-time data, you see:

The difference isn’t just convenience — it’s the difference between intelligence and history.

Large institutional trades can move markets. When a fund executes a block trade for millions of shares, several things happen simultaneously:

1. Immediate Price Impact: Even in dark pools, large trades can influence public exchange quotes as market makers adjust their best bid/ask.

2. Algorithm Response: Other algorithms detect unusual volume patterns within seconds and may adjust positioning.

3. Level Formation: Repeated institutional activity at specific price levels creates support and resistance zones that persist for days or weeks.

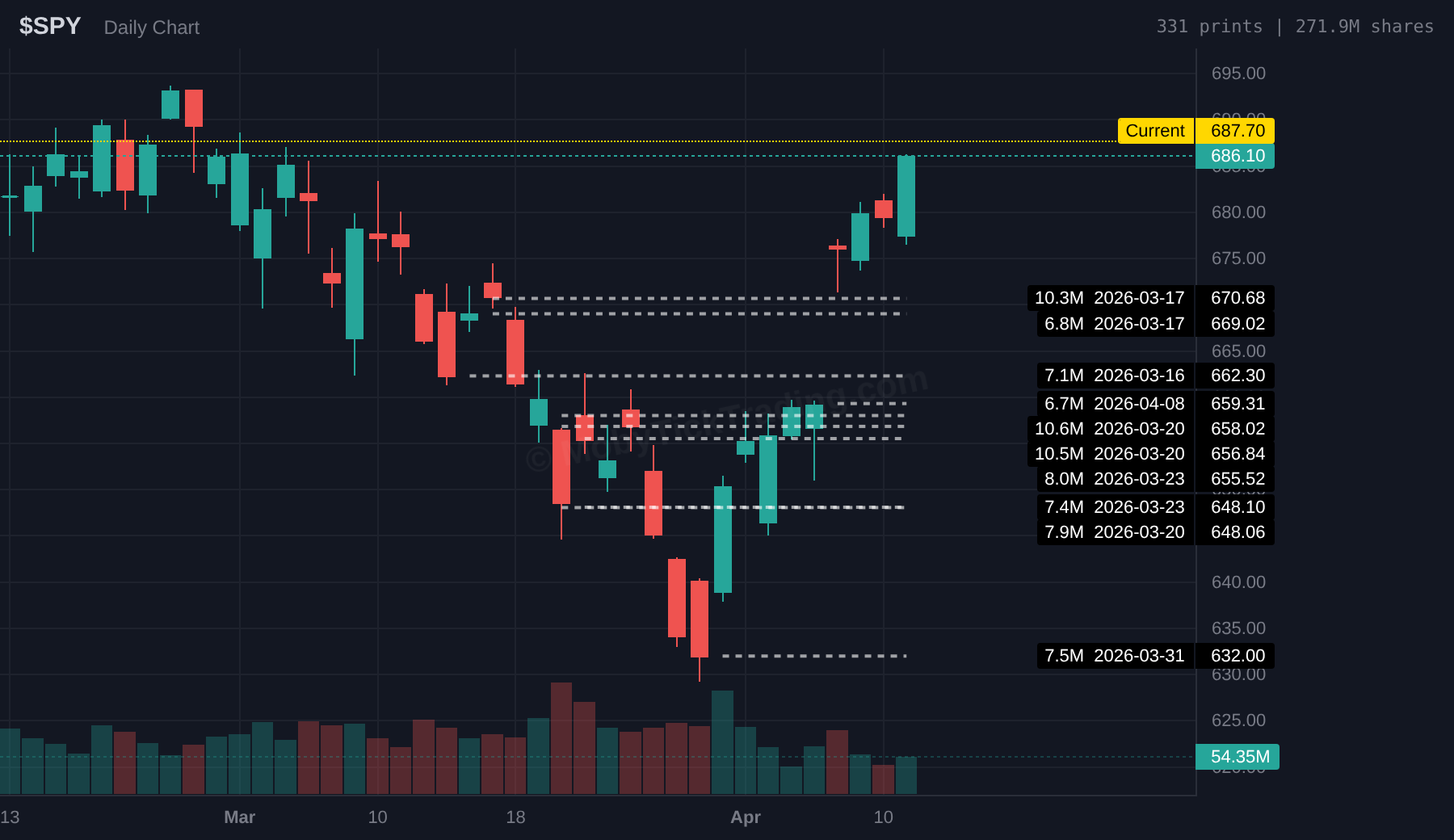

Dark pool data from March 20, 2026 illustrates this clearly. On a day when the broad market showed weakness, dark pool prints revealed significant institutional activity across multiple stocks:

| Ticker | Shares | Price | Dollar Value | Significance |

|---|---|---|---|---|

| SPY | 10.6M | $658.02 | $6.96 billion | Largest 90-day print |

| NVDA | 26.4M | $172.70 | $4.55 billion | Largest 90-day print |

| AAPL | 14.4M | $247.99 | $3.56 billion | 2nd largest 30-day print |

| MSFT | 7.3M | $381.87 | $2.77 billion | Largest 30-day print |

| MU | 4.5M | $422.90 | $1.92 billion | Largest 30-day print |

| AMZN | 7.1M | $205.37 | $1.45 billion | Largest 30-day print |

| JPM | 3.9M | $286.56 | $1.12 billion | Largest 30-day print |

Five of the seven stocks above had their largest dark pool prints of the tracked period on the same day — March 20. A trader with real-time dark pool data would have observed this institutional activity as it happened.

With delayed data? Much of that signal has already been incorporated into price by the time it arrives.

When institutions repeatedly execute large trades at specific price levels, those levels become significant. Real-time data lets you:

Understanding the magnitude of institutional flow helps contextualize market moves. Is today’s rally supported by institutional participation? Is the sell-off seeing institutions active, or just retail activity?

When dark pool activity concentrates in specific sectors across multiple stocks, it may signal rotation in progress. The March 16-20 window showed this pattern clearly across semiconductors:

No single public chart shows this. Real-time dark pool data makes it visible.

Real-time platforms let you set alerts based on criteria that matter to your strategy:

Every minute that passes between a dark pool execution and when you learn about it is a minute the market uses to price in that information. Consider:

By the time delayed data arrives, the informational edge is reduced. You’re not trading on intelligence—you’re trading on recent history.

MobyTick provides institutional-grade dark pool data to retail traders, narrowing the information gap between retail and institutional traders.

Starting at $19.99/month.

In modern markets, the playing field will never be perfectly level. Institutions will always have advantages in capital, research, and execution. But access to real-time dark pool data narrows that gap significantly.

The difference between seeing a $6.96 billion SPY print as it happens versus 10 seconds later isn’t just about opportunity — it’s about understanding market dynamics in real time, forming better hypotheses, and making more informed decisions.

Real-time dark pool data transforms institutional flow from a historical curiosity into actionable intelligence. In a market where milliseconds matter, that transformation is everything.

Ready to see institutional flow in real-time? Visit MobyTick Trading to start your free trial and access the same dark pool intelligence used by serious traders.

Data verified against MobyTick API as of April 14, 2026. All dollar values represent aggregate dark pool print values from FINRA Trade Reporting Facility data.

Keywords: real time dark pool, live dark pool data, institutional flow, dark pool trading, block trade analysis, institutional trading data