Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Learn what late prints are in dark pool data, why they matter in SPY, QQQ, IWM, and DIA, and how MobyTick separates delayed-reported ETF flow from real-time institutional activity.

What Are Late Prints?

Late prints are dark pool trades that can legally be reported up to approximately 24 hours after execution. Unlike standard block trades that appear in near real time, late prints hit the tape after the transaction window has already closed.

The key distinction is this: the print is real, but the timing of the report is delayed. The volume already belonged to the previous days session — it should not be interpreted as fresh real-time institutional activity entering the market at the moment it appears on the tape.

In plain English: If you see a large dark pool print on the index ETFs that is usually not withing the current day’s trading range, you can build an entire trade thesis around a signal that is already stale relative to current price action.

That is why separating late prints from real-time block flow matters. They answer two different questions:

The second question is the one most traders forget to ask. This guide is designed to make sure you don’t.

Moby Tick tracks late prints separately from the broader dark pool tape across ~10,000 names. Late prints on SPY, QQQ, IWM, and DIA tend to report with 4-decimal-place precision and stack at identical prices across many transactions. That signature is how we identify and aggregate them into single “trade events” at a given level.

This separation helps traders distinguish delayed reporting from current-session real-time flow — a distinction that is the difference between context and confusion when reading the institutional tape.

These four ETFs are the most widely traded institutional vehicles in the market. They are natural places for broad exposure, basket trading, and large off-exchange positioning. When large block trades in these names report late, the dollar values can run into the billions. That makes the late-print record on these ETFs especially useful for forward support and resistance analysis.

Moby Tick tracks them because the concentration of institutional flow in these names means the delayed-reporting signal carries more weight — and the footprint is more reliable — than scattered prints across smaller names.

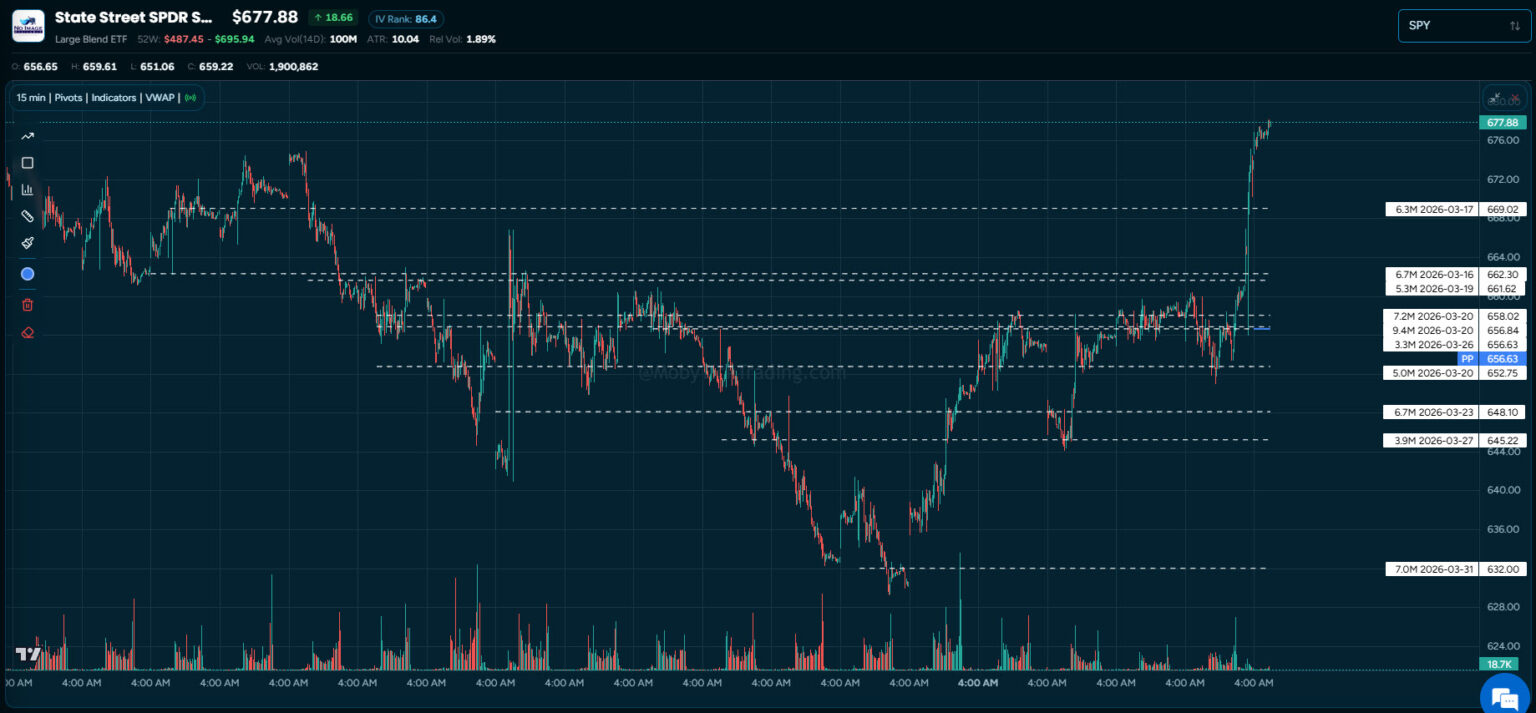

On March 31, 2026, SPY opened at $638 on a decisively bearish day. Late prints reported a $4.7 billion trade at $632 — 7.5 million shares, below the open, at a level price never traded during that session. SPY closed above prior late print levels the same day.

By April 8, the cumulative late print position at and around that level had grown to 42.7 million shares totaling $27.7 billion across 10 trades. Institutions were not just buying the dip — they were stacking size. The gap up on April 8 confirmed it.

From there, another 18.8 million shares were added between $701.75 and $711.27 as the move extended. That is accumulation behavior, not distribution.

Friday, May 15 printed $4.1 billion at $748.11 — 5.5 million shares, $4.65 above the day’s high of $743.46. Price never traded there during regular hours. This trade represented 8.99% of the entire daily volume for SPY.

The white dotted lines on the chart mark price levels where late prints landed but the tape never went during regular trading. Across five trades in the week, total activity reached 18.7 million shares and $13.8 billion in notional value. These levels become forward support and resistance.

The levels identified through late prints hold up intraday the same way they hold up on the daily chart. That consistency is what makes them most useful for active traders: the institutional footprint does not care about your chart settings.

Late prints are one of the most valuable windows into institutional behavior — when you understand the reporting delay and separate it from real-time activity. The footprint reveals where smart money was positioned before the broader market caught on, and the levels hold across every timeframe.

For a live view of late prints and the full institutional dark pool tape, visit MobyTick Trading.

Disclaimer: This content is for educational and informational purposes only. It does not constitute financial advice, trading recommendations, or a solicitation to buy or sell securities. Past performance and historical data are not indicative of future results. Always conduct your own due diligence before making trading decisions.